Harnessing the Advantages of the ROBS / BORSA Structure.

PART I: C-CORP

By: Bryan Uecker, QPA, QPFC, AIF, AIFA

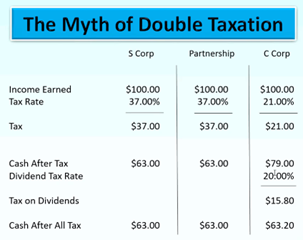

ROBS (Rollover as Business Start-up) or BORSA™ (Business Owners Retirement Savings Account) structures are exclusively compatible with C-Corps. This is because only C-Corps permit a 401(k) profit-sharing plan to serve as a shareholder. Upon discovering this exception, some prospective clients may feel disappointed, as the C-Corp often carries a stigma of “double taxation”. Historically viewed as “the entity choice of last resort” due to potential for double taxation resulting from corporate-level taxes and subsequent taxation upon distribution or liquidation. The good news is that C corporations present unique tax advantages that S corporations and partnerships cannot replicate.

To debunk the stigma of “double taxation” right up front, a helpful chart compares the corporate tax and dividend tax to profits through a pass-through entity at a personal tax rate of 37%:

So the issue is not how many times you are taxed……but rather how much tax you pay.

Now that we have cleared up the myth, here are ten benefits of a C-Corp:

1. Lowering Overall Tax Burden: C Corps can achieve significant tax savings thanks to a single flat corporate tax rate of 21%. By proactively managing dividends and salaries, business owners can optimize their tax burden, generally resulting in lower overall taxes than pass-through entities.

2. Flexible Fiscal Year: C Corps can choose their fiscal year, unlike LLCs and S Corps. This allows for better timing of income recognition and expense deductions, enabling shareholders to further minimize their tax burden.

3. Retaining Earnings for Growth: C Corps can reinvest profits within the company at a lower tax cost. Unlike S Corps, where profits are passed through to shareholders and taxed regardless of distribution, C Corps can retain earnings to fuel future expansion without immediate tax consequences.

4. Deducting Salaries and Bonuses: Shareholders of C Corps can receive salaries and bonuses, which are deductible expenses for the corporation. Businesses can optimize tax efficiency and mitigate double taxation concerns by structuring compensation packages appropriately.

5. Tax Write-offs for Fringe Benefits: C Corps can deduct 100% of medical premiums and other fringe benefits provided to employees. This includes health, long-term care, and retirement plan contributions, offering substantial tax savings opportunities for the corporation and its employees.

6. Charitable Contributions Deduction: C Corps can deduct charitable donations as business expenses, subject to certain limitations. This benefits worthy causes and provides tax advantages for the corporation, with the option to carry over excess contributions to future tax years.

7. Gaines: C Corps are taxed at a flat 21% on short-term and long-term gains so you no long have to carry economic risk to get to a lower tax bracket. You sell you capital asset when it is best for you. C Corps can carry forward capital and operating losses indefinitely to offset future profits. This flexibility allows businesses to smooth out tax liabilities over time, particularly during growth or economic downturns.

8. Fewer Ownership Restrictions: Unlike S Corps, which have strict ownership rules, C Corps can have unlimited shareholders, issue multiple classes of stock and be owned by anyone or anything. This flexibility facilitates equity financing and business expansion without the constraints imposed by S Corp regulations.

9. Favorable Treatment for Passive Investors: Passive investors in C Corps benefit from the inability to pass losses through to individual tax returns. Unlike S Corps, where active participation is required to claim losses, passive investors can still enjoy tax advantages without direct involvement in management.

10. Unique Financing Opportunities: Registering as a C Corp opens doors to diverse financing options, including public offerings and innovative strategies like 401(k) business financing, such as ROBS or BORSA™ plans. These financing avenues give businesses access to capital while minimizing debt obligations, offering a valuable alternative to traditional lending sources.

With over four decades of experience, DRDA, LLC has focused on supporting entrepreneurs in initiating, expanding, and selling their businesses. Leveraging our proficiency in accounting, business consulting, and retirement plan design, we harness the advantages of the ROBS/BORSA™ structure to benefit our clients throughout the operation of their business and at their succession transition or exit of their business, not just at formation.

By: Bryan Uecker, QPA, QPFC, AIF, AIFA

- Published in Business Lending, ROBS 401(k), ROBS 401k Provider, Small Business, Starting a Business

Lost Your Job Due to The Pandemic? Start, Purchase or Fund your own business today.

Lost your job due to the pandemic? You’re not alone.

Research shows that, as of July 2021, unemployment rates have not yet recovered (5.4% vs. 3.5% pre-pandemic). There’s no better time to get started investing in your own business with DRDA’s BORSA™ plan.

Avoiding Early Withdrawal Taxes & Penalties

Normally, if you withdraw money from your 401(k) before the age of 59½, you are liable to pay income taxes and a 10% early withdrawal penalty on your money. The Business Owners Retirement Savings Account will allow you to take control of your 401(k), IRA, or other qualified funds and use them to start, purchase, or fund a business tax or penalty free.

What types of funds are eligible?

Not only does the BORSA™ Plan work with a traditional 401(k), DRDA can also assist you with rolling over the following into a business:

- 401(a)

- 403(b)

- 457

- IRAs ( with exceptions for Roth or Non-spousal inherited IRAs)

- Pension

- Profit Sharing

- ESOP

- Annuities

- Thrift Savings Plans

I’m ready to start my business! How does this process work?

- Form a new C Corporation

- The new C Corp. will establish a 401(k) Profit Sharing plan

- Existing retirement funds will be rolled over into the new 401(k) plan

- Participants in the 401(k) plan will invest in stock of the newly formed C Corp.

This process typically takes around 30 days from the initial engagement, to the time you will receive your funds in hand.

Have more questions, comments, or are you ready to get started?

If you’re ready to get started or have any additional questions, please register for our FREE webinar (September 8th, 1pm CST & September 9th, 5pm CST) below:

- Published in Business Lending, ROBS 401(k), ROBS 401k Provider, Uncategorized

Finance Your New Business During the Pandemic

BORSA, finance your new business during the pandemic

How can you make BORSA work for you? Now may be a great time to explore ROBS, or the Rollover Business Startup Solution and what it can do for you during the pandemic.

Key Points

- Start a new business or franchise

- Legally pay yourself a salary

- Abide by IRS and ERISA guidelines

What is the BORSA Plan?

The BORSA (Business Owners Retirement Savings Account) is DRDA’s, LLC Solution otherwise known as ROBS (Rollover Business Startup Solution), an IRS and ERISA approved structure that allows investors to use their retirement funds for a new business or franchise that they will be personally involved in. It is the primary way a retirement plan holder can have personal involvement in a business utilizing their retirement funds, without triggering IRC prohibited transaction rules.

Setting up a BORSA Plan requires planning but can be accomplished in relatively few steps.

- Set up a C Corporation – The process begins by establishing the new corporation, using the proper legal structure to support the establishment and operation of the company’s qualified retirement plan.

- Rollover your funds – Transfer your funds from an old IRA or 401(k) plan into a new 401(k) plan that the stock of the start-up C corp. business sponsors or adopts.

- Start earning a salary – You must be an employee of your new business and provide a legitimate service. Your compensation must come from your business.

How Do BORSA and Pandemic Relate?

While there’s a pandemic, millions are losing their jobs and joining the ranks of the unemployed. More than ever, many are trying to rely on themselves and not some corporate entity that must make difficult decisions to comply with federal and state mandates affecting individual earning, security, and livelihood. Using BORSA can be an ideal way to start the business of your dreams with money you already have.

BORSA can help you fund a new business or franchise with retirement funds, and that means you’re starting on your way to owning and fulfilling your goals. When COVID-19 hit, no one could have anticipated it would bring the unprecedented upheaval of everyday life that it has.

How Does BORSA Work?

The BORSA Plan allows an investor to create a C Corporation, and the C Corp’s profits are taxed separately from the owner as it is owned by shareholders. Next, funds are transferred from an old IRA or 401(k) plan. Then, as an employee providing a legitimate service, you are able to earn a salary at the business you’ve created.

There are very specific IRS and ERISA rules that have to be followed, and for this reason guidance is recommended. DRDA, LLC can help you get started. When it’s time for your new company’s stock to get valuated by the IRS, DRDA, LLC will help value the stock of the new or existing company.

BORSA Benefits

More than almost anything else, Americans are looking to make certain they can make it through the pandemic, civil unrest, and the whole of the current situations currently embroiling the nation. For those who have lost their jobs and have been unable to find replacement work, tapping into their retirement funds have been one source of income to help. But what happens when the funds have been depleted?

More than just taking funds out, though, BORSA can help you open a franchise or start a new business you can own yourself. Your money is helping you and your family first. The primary benefit of using the BORSA Plan is that you can employ it to use your retirement funds to invest in a business you will be personally involved in. You can do this without paying tax on the retirement funds you wish to use as a distribution.

Additionally, investing in yourself within your retirement portfolio is an excellent way to diversify. Your investments in traditional assets such as stocks and bonds, and alternative assets such as cryptocurrency, exist separately, and you can fund your own business as well. This may protect investment portfolios as a whole during times of unrest and market volatility,

During the COVID-19 and now the Delta Variant financial crisis, it’s important to know where your money is and what it’s doing. While investing in the market and traditional assets can bring you financial success, it’s very volatile at this time. Alternative assets like real estate can help diversify your portfolio. And using the BORSA Plan to fund your dreams can help you even more.

If you are interested in receiving more information on the BORSA™ plan, DRDA, LLC will be hosting a webinar on September 8th and 9th, 2021.

Click Here to sign up and access this FREE webinar.

- Published in Business Lending, ROBS 401(k), ROBS 401k Provider, Small Business, Starting a Business, Uncategorized

Paycheck Protection Program Loan Forgiveness

Small Businesses who received Paycheck Protection Program loans can prepare for the process of having the debt reduced or even wiped clean with the forgiveness application released by the Small Business Administration on Friday May 15,2020.

SBA said it planned to release official regulations and guidance soon. But the form might help employers by offering reminders of the rules as well as what appears to be some new guidance on how the government will handle loan forgiveness.

According to a SBA news release Friday:

The form and instructions include several measures to reduce compliance burdens and simplify the process for borrowers, including:

• Options for borrowers to calculate payroll costs using an “alternative payroll covered period” that aligns with borrowers’ regular payroll cycles

• Flexibility to include eligible payroll and non-payroll expenses paid or incurred during the eight-week period after receiving their PPP loan

• Step-by-step instructions on how to perform the calculations required by the CARES Act to confirm eligibility for loan forgiveness

• Borrower-friendly implementation of statutory exemptions from loan forgiveness reduction based on rehiring by June 30

• Addition of a new exemption from the loan forgiveness reduction for borrowers who have made a good-faith, written offer to rehire workers that was declined (Minor formatting edits.)

“The Treasury Department and Small Business Administration released a loan forgiveness application form for the CARES Act’s Paycheck Protection Program (PPP), which had been urgently sought by CPA firms and their small business clients in recent weeks,” the American Institute of CPAs wrote in a news release Saturday. “The document and related instructions partially address some outstanding issues but leave others unaddressed and, more importantly, still do not provide enough flexibility for those who receive funds, according to the American Institute of CPAs. Download the PPP Forgiveness Loan calculator from the American Institute of CPAs.

The SBA opened the PPP process on April 3. Small Businesses who managed to obtain the PPP loans in the early days of eligibility are coming up on the eight-week (current to 6-7 weeks in) “Covered Period” to have spent the money, which means some might want to get the ball rolling on the forgiveness process for peace of mind. (The deadline to apply for forgiveness is unclear, but the form carries an Oct. 31 expiration date.) Otherwise, the loans carry 1 percent interest and mature in two years.

The eight-week “Covered Period” starts ticking either on the day you received loan dollars, but the feds say they’ll also allow employers to key off of their first pay period after receiving the loan — within limitations. For example, the 25 percent of the loan which can be spent on eligible non-payroll costs like rent must have been spent during the “Covered Period.”

“For administrative convenience, Borrowers with a biweekly (or more frequent) payroll schedule may elect to calculate eligible payroll costs using the eight-week (56-day) period that begins on the first day of their first pay period following their PPP Loan Disbursement Date (the ‘Alternative Payroll Covered Period’). For example, if the Borrower received its PPP loan proceeds on Monday, April 20, and the first day of its first pay period following its PPP loan disbursement is Sunday, April 26, the first day of the Alternative Payroll Covered Period is April 26 and the last day of the Alternative Payroll Covered Period is Saturday, June 20,” the form states. “Borrowers who elect to use the Alternative Payroll Covered Period must apply the Alternative Payroll Covered Period wherever there is a reference in this application to ‘the Covered Period or the Alternative Payroll Covered Period.’ However, Borrowers must apply the Covered Period (not the Alternative Payroll Covered Period) wherever there is a reference in this application to ‘the Covered Period’ only.”

The government will also accept the spending if costs are incurred during the time frame and paid by the first payday or billing date after it.

“Borrowers are generally eligible for forgiveness for the payroll costs paid and payroll costs incurred during the eight-week (56-day) Covered Period (or Alternative Payroll Covered Period) (‘payroll costs’),” the form states. “Payroll costs are considered paid on the day that paychecks are distributed, or the Borrower originates an ACH credit transaction. Payroll costs are considered incurred on the day that the employee’s pay is earned. Payroll costs incurred but not paid during the Borrower’s last pay period of the Covered Period (or Alternative Payroll Covered Period) are eligible for forgiveness if paid on or before the next regular payroll date. Otherwise, payroll costs must be paid during the Covered Period (or Alternative Payroll Covered Period). …

“An eligible nonpayroll cost must be paid during the Covered Period or incurred during the Covered Period and paid on or before the next regular billing date, even if the billing date is after the Covered Period. Eligible nonpayroll costs cannot exceed 25% of the total forgiveness amount. Count nonpayroll costs that were both paid and incurred only once.”

The government will forgive the loan and any interest if at least 75 percent of the money received had been spent on payroll and the remainder spent on rent, utilities or mortgage interest, according to the form. The maximum forgivable amount per employee maxes out at what would work out to $100,000 a year in pay.

The amount forgiven will be decreased proportional to the drop-in workforce and potentially pay. The government will let pay cuts slide if employees made at least 75 percent of what they averaged between Jan. 1 and March 31 or were paid between Feb. 15-April 26, the average salary or hourly wage they were making as of Feb. 15, according to the new form. Borrowers that cut pay more than the government would like can receive a pass if they restore paychecks to Feb. 15 levels by June 30.

The government also will let layoffs slide and forgive the full loan if you laid off people between Feb. 15-April 26 and brought your workforce to Feb. 15 levels by June 30, according to the form. It also grants an exemption to an employer who fired employees for cause or “made a good-faith, written offer” to rehire a worker only to have the employee decline. Exemptions also exist if the employee quit voluntarily or asked for their hours to be reduced. “Any FTE reductions in these cases do not reduce the Borrower’s loan forgiveness,” the form states.

Congress appropriated hundreds of billions for PPP small business loans over the course of two separate bills, resulting in a PPP “Phase One” and “Phase Two.” The forgivable loans were seen as a means of helping small businesses preserve jobs after the national COVID-19 coronavirus response shattered the economy.

PPP “Phase One” saw another more than $342 billion net dispensed in nearly 1.7 million loans made by 4,975 lenders, according to the SBA. The average “Phase One” loan came out to $206,000. Nearly 26,000 loans exceeding $2 million had been issued in Phase One; these represented 1.57 percent of the loan applications approved, but nearly 28 percent of the loan dollars.

After the PPP program ran out of money (lawmakers approved $349 billion), Congress approved more funds for what became “Phase Two.” Generally speaking, you can borrow the equivalent of 10 weeks of payroll.

As of 5 p.m. Saturday May 16,2020, 5,479 “Phase Two” lenders had issued nearly $195.2 billion across nearly 2.8 million loans. The average “Phase Two” loan worked out to $70,622.

More information:

PPP loan forgiveness application and instructions

Small Business Administration, May 15, 2020

“AICPA Says Treasury and SBA PPP Loan Forgiveness Application Leaves Many Questions”

American Institute of CPAs, May 16, 2020

SBA “Coronavirus Relief Options” page

SBA Paycheck Protection Program (PPP) webpage

List of PPP lenders in your state

Paycheck Protection Program FAQs

SBA, May 13, 2020

- Published in Business Lending, Small Business

Payroll Protection Program (PPP) to relaunch Monday April 27, 2020

DRDA continues to provide you information as quickly as we can related to any tax law changes, as well as financial aid and loan opportunities as a result of the COVID-19 crisis. As you can imagine, this is a rapidly changing environment and we will continue to disseminate information as it is made available to us.

On March 27th 2020, President Trump enacted the Coronavirus Aid, Relief, and Economic Security (CARES) Act to Help small businesses keep workers employed through a program known as the Paycheck Protection Program (PPP). Which allowed banks to issue SBA 100% federally guaranteed loans to small businesses that can attest to suffering economic hardship as a result of the COVID-19 crisis. Importantly, these PPP loans may be forgiven if borrowers maintain their payrolls during the crisis or restore their payroll afterward.

Yesterday April 23, 2020 Congress approved an additional $310 billion in Funding to replenish the PPP Program which has run out of money. Congress had allotted an initial $349 billion in the last relief bill, a $2.2 trillion package enacted on March 27, only to see the funds run dry shortly afterward due to the rush of businesses seeking to tap the benefits.

Banks will start processing application Monday April 27, 2020. We anticipate the money to move very quickly. We suggest to those applying for the PPP, to do so as soon as possible, and be ready to submit their applications immediately as the program becomes available.

Here is a link to a small business guide published yesterday by the U.S Chamber of Commerce. Please take the time to read this memo, and if you believe your business qualifies (if you need help in that determination, please let us know), then you need to contact your banker to start the process. Please keep in mind, these loans are moving very fast and they are being created as a “first come, first served” priority list for applicants. This will typically be a bank process, not an accounting process, so submitting a loan application through your bank will be of the utmost importance.

The last twelve (12) months payroll information will be needed. It is our understanding at this time, that payroll will include wages, employer paid payroll taxes, health insurance premiums and retirement expense (i.e. 401(k) match).

As stated previously, for the PPP loan to be forgiven your business will have to prove that it retained and continued to pay employees. The rules are still evolving regarding the employee retention provision but understand that employee retention is paramount to having this loan forgiven.

The administration’s PPP program guidelines can be found at www.treasury.gov, and the U.S. Small Business Administration’s search tool to find a bank that offers PPP loans can be found at www.sba.gov/paycheckprotection/find.

We hope that you are well, and please stay safe. Please don’t hesitate to contact us with any questions you may have.

- Published in Business Lending, Small Business, Tax

Your BORSA Plan and the CARES Act

On March 27, 2020, the Coronavirus Aid, Relief, and Economic Security (CARES) Act was enacted to address the

financial difficulties that have resulted from the COVID‐19 pandemic. Included in this law were provisions that

provide special coronavirus related distributions (CRD) for qualifying plan participants. Below is a brief summary of the new CRDs available and new loan provisions to qualifying participants.

Coronavirus Related Distribution:

Qualifying participants can request a distribution of up to $100,000 from the retirement plan without incurring a

10% early distribution penalty. There is no age requirement and you can take coronavirus‐related distributions

whether actively employed or not. You can request the entire amount in a one lump sum, or multiple payments, but all must be taken by no later than December 30, 2020.

There is a federal tax withholding requirement of 10%, but you may choose to waive it completely or withhold a

different amount at the time of distribution. The amount of distribution is subject to federal tax, but you will be able to spread the taxes owed on the distribution over three years.

You may repay the entire amount distributed to you within three years. This opportunity allows you to repay

some or all of the distribution to any qualified plan or IRA that accepts rollovers as a way to minimize your income

tax liability. This is different than a loan in that there is no interest and no periodic payment requirement, and the

ability to repay does not require an election at the time of distribution. Repayment can be in a single lump sum or

via installments of different amounts at different times, but the repayment window only runs for three years from

the date you first receive the distribution.

It is important to emphasize that this new CRDs only apply to individual plan participants that meet certain requirements. If you should choose to utilize either of these provisions, you must certify that you meet one or more of the conditions listed below.

You have experienced adverse financial consequences as a result of:

• having been diagnosed with SARS‐CoV‐2 or COVID‐19 by a test approved by the Centers for Disease Control and

Prevention,

• a spouse or other dependent (as defined in section 152 of the internal revenue code) being diagnosed with

SARS‐CoV‐2 or COVID‐19 by a test approved by the Centers for Disease Control and Prevention,

• being quarantined,

• being furloughed,

• being laid off or having work hours reduced,

• being unable to work due to a lack of childcare,

• being an owner of a business who has had to close the business or reduce hours worked in the business due to

the COVID‐19 virus.

Increase of Maximum Loan Amount

Under current rules the maximum loan amount available is the lesser of 50% of vested account balance or $50,000

reduced by the highest outstanding loan amount in the previous 12 months. The new rule increases the maximum

loan amount to the lesser of 100% of vested account balance or $100,000 reduced by the highest outstanding loan

in the previous 12 months. This provision has been incorporated into our plan but will expire on September 23, 2020.

The loan must still meet all other requirements and limitations set forth under the plan.

Loan Payment Suspension

Qualifying participants who currently have loans outstanding or who take new loans can suspend their loan

payments for the remainder of 2020. It is important to know that interest will continue to accrue on any loan where

payments are suspended.

Re‐Amortization of Loans with a Final Payment Date that is Later than 12/31/2020:

If a loan is suspended under

this provision, the loan will be re‐amortized to include the accrued interest and extend the loan duration for 12

months beyond the original final loan payment date. This re‐amortization will result in a new loan payment amount.

Payments, using this new payment amount, will begin as of the first payment due date in 2021.

Example: Loan with an original first payment date of 3/15/2018 with a final payment date of 3/15/2021. Payment

is suspended as of 4/15/2020 for the remainder of 2020. New payment is calculated by including the accrued

interest for the period 4/15/2020 through 12/31/2020 and by extending the final payment date to 3/15/2022.

Payments resume on 1/15/2021, using the new payment amount.

Re‐Amortization of Loans with a Final Payment Date of prior to 12/31/2020:

If a loan is suspended under this

provision, the loan will be re‐amortized to include the accrued interest and extend the loan duration for 12 months

beyond the original final loan payment date. This re‐amortization will result in a new loan payment amount.

Payments, using this new payment amount, will begin 12 months after the date of the suspension.

Example: Loan with an original first payment date of 9/30/2017 with a final payment date of 9/30/2020. Payment

is suspended as of 4/15/2020 for the remainder of 2020. New payment is calculated by including the accrued

interest for the period 4/15/2020 through 3/31/2021 and by extending the final payment date to 9/30/2021.

Payments resume on 4/15/2021, using the new payment amount.

Please note that this document was prepared based on our best interpretation of the law. Additional guidance from regulators is likely. This guidance may result in the information presented in this document being inaccurate.

If we receive information that is conflicting with what we have stated here we will send that information to you and post it on our website www.drdacpa.com. In the interim, please call us if you have any questions or if we may be of any assistance.

- Published in Business Lending, ROBS 401(k), ROBS 401k Provider, Small Business

COVID-19 – Small Businesses the SBA programs, and the CAREs Act.

Our world is going through unprecedented times. The COVID-19 virus is not only a healthcare crisis but an economic crisis as well affecting millions of small businesses, their owners, and employees.

DRDA CPAs & Business Consultants care about you, your family, and your business. We are hard at work – remotely – to continue to find the best solutions for our clients.

On March 27th the President signed into law the CAREs Act which contained $376 billion in relief for American workers and small businesses.

It was a historic undertaking and the SBA processed more loans in two weeks than they would in 20 years. Programs are now out of money. It is anticipated that Congress will appropriate more funds, maybe as early as this week.

In the meantime, we wanted you to have this information:

• PPP & EIDL programs are out of money

• Banks and SBA are not currently taking applications

• Congress will appropriate more money

• If you did not get your money from the first allocation you MUST be ready for the next one – now is the time to complete the gathering of your information so your application can be submitted the day the programs reopen

What you can do in the interim:

• CAREs Act allows you to borrow up to $100,000 from your 401k

• You can utilize a BORSA Plan [brief description of BORSA] or if you are already a BORSA client you could roll more funds (if you have them available) into your plan and invest into your C Corp

• Line of Credit with your Bank

• Unemployment

DRDA continues to monitor the situation on an hour by hour basis. We’ve hosted several webinars over the last two weeks and will start those back up once the programs get refunded. You can register for webinars on our main site DRDACPA.com. We are also blogging the latest information we have.

If we can help please reach out – you can call me direct if you’d like 281-954-6023 or email suzy@drdacpa.com

- Published in Business Lending, ROBS 401(k), Small Business

Everything You Need to Know About Coronavirus Federal Small Business Stimulus Aid Programs

A breakdown of all the federal programs and aid for small business coronavirus assistance.

Three separate packages approved by Congress and signed by President Trump over the past weeks combined offer a variety of assistance to businesses. Here’s a breakdown of what’s in those packages and how your business can take advantage of these relief efforts.

Coronavirus Preparedness and Response Supplemental Appropriations Act

What is it?

Signed into law on March 6, The Coronavirus Preparedness and Response Supplemental Appropriations Act provides $8.3 billion in emergency funding for federal agencies to respond to the coronavirus outbreak, enabling the U.S. Small Business Administration to offer $7 billion in disaster assistance loans to small businesses impacted by COVID-19.

What does it mean for small business?

The SBA is offering designated states and territories low-interest federal disaster loans to small businesses suffering substantial economic harm as a result of the coronavirus.

These loans may be used by small businesses to pay fixed debts, payroll, accounts payable and additional bills that can’t be paid because of COVID-19’s impact. The interest rate is 3.75% for small businesses without other available means of credit. The interest rate for non-profits is 2.75%. Businesses with credit available elsewhere are not eligible.

The SBA loans come with long-term repayments, up to a maximum of 30 years, in an effort to keep payments affordable. Loan terms are determined on a case-by-case basis, according to individual borrower’s ability to repay.

The SBA has amended its disaster loan criteria to help borrowers still paying back SBA loans from previous disasters. By making this change, deferments through December 31, 2020, will be automatic. Hence, borrowers of home and business disaster loans do not have to contact SBA to request deferment.

Where can I learn more?

SBA Coronavirus Small Business Loan Page

Coronavirus (COVID-19): Small Business Guidance & Loan Resources

Families First Coronavirus Response Act

What is it?

Signed into law on March 18, the Families First Coronavirus Response Act (FFCRA or Act) contains eight divisions designed to provide assistance to covered employees and households with eligible children affected by COVID-19. Key components of the Act include:

- Mandatory emergency paid sick leave for covered employees who, as a result of COVID-19, are quarantined, symptomatic or caring for a symptomatic individual, or caring for a child whose school has been closed.

- An expansion of unemployment benefits.

- Modifications to the USDA nutrition and food assistance programs.

- New requirements for coronavirus diagnostic testing.

- A temporary increase in the Medicaid federal medical assistance percentage (FMAP).

What does it mean for small business?

The FFCRA affects small businesses in two key ways:

- Paid sick and family leave. The law requires all private businesses with fewer than 500 employees to provide emergency paid sick or family leave for employees affected by the coronavirus outbreak.

- Employer tax credits. The law provides employers

with fewer than 500 employees with refundable payroll tax credits to cover the

cost of providing the paid sick leave and the paid FMLA leave to their

employees. Specifically, the law states that:

- Employers will receive 100% tax credit against their payroll tax liability up to the capped amount of benefits they must pay.

- Health insurance costs are also included in the credit.

- Self-employed individuals receive an equivalent credit.

- If an employer is owed more than the capped amount and a refund is owed, the IRS will send the refund as quickly as possible.

- Reimbursement will be quick and easy to obtain.

Where can I learn more?

- The full text of the Act can be found at Congress.gov.

- For additional information regarding the mandatory emergency paid sick leave, see this detailed guide provided by the U.S. Department of Labor.

Coronavirus Aid, Relief, and Economic Security Act (CARES Act)

What is it?

The CARES Act, which is expected to be passed by both houses of Congress and signed by the President in the near future, has a number of components aimed at helping small businesses survive and recover from losses suffered during the coronavirus outbreak. Key components of the CARES Act include a loan program from the SBA, changes to unemployment benefits and changes to business tax filing requirements.

What does it mean for small business?

Anticipated key components of the CARES Act include:

- Small Business Paycheck Protection Program: A new lending program that allows businesses to borrow enough to cover monthly payroll costs for businesses for up to 2.5 months. If used for payroll, mortgage interest or other qualified expenses, these loans will be forgiven as long as the employer continues to employ its workers or rehires them when they reopen for business.

- Business tax provisions: Employers can defer payment of the employer share payroll taxes.

- Payments for individuals: It is anticipated those who make less than $75,000 a year will receive direct payments of $1,200 per individual ($2,400 joint return) plus $500 per child. This will phase out for incomes above $75,000 ($150,000 joint filings).

- Unemployment assistance: If your business is closed because of coronavirus and your employees cannot work from home, or your employees are unable to work due to illness or the need to take care of someone who is ill with the virus, they can collect unemployment.

Where can I learn more?

Small Business Administration’s COVID-19 page

More info on IRS tax changes can be found here.

More information on filing for unemployment assistance can be found at the U.S. Department of Labor, though you or your employees will need to file through your state’s unemployment program.

- Published in Business Lending, Small Business, Tax