Comparing Self-Directed IRAs vs. BORSA/ROBS

By: Bryan Uecker, QPA, QPFC, AIF, AIFA

Self-directed IRAs and BORSA/ROBS (Rollovers for Business Start-ups) offer distinct approaches to investing in businesses:

Business Involvement

BORSA/ROBS: Requires active participation in business operations, including receiving a salary if deemed reasonable. Structured through a C corporation, which is the sponsor of the retirement plan.

Self-directed IRAs: Passive investment vehicles where IRA owners cannot engage in business management or take salaries. Doing so could violate IRS rules on prohibited transactions.

Tax Considerations

BORSA/ROBS: Subject to regular corporate taxes; UBIT (Unrelated Business Income Tax) does not apply since the C corporation is taxable.

Self-directed IRAs: Income from business activities may trigger UBIT if unrelated to the IRA’s tax-exempt purpose.

Loan Guarantees

BORSA/ROBS: Allows funds to be used as a down payment for business loans, including SBA loans.

Self-directed IRAs: Cannot guarantee loans, maintaining separation between IRA assets and personal liabilities.

Ownership Flexibility

BORSA/ROBS: Enables up to 100% ownership of the business, providing full control.

Self-directed IRAs: Direct ownership risks violating IRA rules if exceeding certain ownership thresholds, jeopardizing tax benefits.

Conclusion: Self-directed IRAs are ideal for passive investors seeking hands-off involvement, while ROBS empowers owners with direct control and tax advantages through a C corporation setup.

- Published in ROBS 401(k), ROBS 401k Provider, Small Business, Starting a Business

Unlocking Success: Navigating the ROBS Journey!

A Persuasive Essay on the Benefits of the ROBS Strategy

By: Eva Jiang, M.B.A., M.S.

Recently, DRDA hosted an enlightening webinar titled “Unlocking Success: Navigating the ROBS Journey,” aiming to demystify the ROBS (Rollover as Business Start-up) strategy for aspiring entrepreneurs. This essay argues that the ROBS strategy offers a unique and advantageous pathway for individuals to leverage their retirement funds to start or buy a business without incurring taxes or penalties. The webinar provided an in-depth exploration of the ROBS strategy, addressing common concerns and illustrating its potential benefits.

Setting the Stage for Success

The webinar began with the foundational steps necessary to ensure a distraction-free environment, emphasizing the importance of focused attention when dealing with complex financial strategies. Attendees were encouraged to silence their phones and find a quiet place, setting the stage for a productive session. The introduction of the Q&A chat box underscored the interactive nature of the webinar, allowing participants to engage directly with the experts, thereby enhancing their understanding of the ROBS strategy.

Expert Insights and Comprehensive Understanding

The session featured two distinguished speakers: Doug Dickey, a Partner at DRDA with credentials such as CPA, CVGA, and CEPA, and Bryan Uecker, the Retirement Plan Manager with qualifications including QPA, QPFC, AIF, and AIFA. Their combined expertise provided a thorough and reliable foundation for understanding the ROBS strategy. This high level of expertise is crucial for individuals considering using their retirement funds to invest in a business, as it ensures that they receive accurate and comprehensive information.

The Mechanics of the ROBS Strategy

Doug and Bryan explained the ROBS strategy in detail, highlighting its core components: forming a C Corporation, establishing a 401(k) Profit Sharing Plan, and rolling over retirement funds into this plan to invest in a new business. This approach allows individuals to use their retirement funds without incurring the taxes and penalties typically associated with early withdrawals. The ROBS strategy thus provides a viable and advantageous option for entrepreneurs who lack sufficient liquid capital but possess substantial retirement savings.

Addressing Common Concerns

A significant portion of the webinar was dedicated to addressing common concerns and questions from the attendees. These included:

Compliance with IRS Regulations: Ensuring compliance with IRS regulations is a primary concern for anyone considering the ROBS strategy. The speakers provided detailed guidance on meeting all necessary requirements, emphasizing the importance of adherence to avoid legal complications.

Eligible Retirement Funds: The types of retirement funds that qualify for ROBS were clarified, providing attendees with a clear understanding of their eligibility.

Tax Benefits: The tax advantages of operating under a C Corporation structure were highlighted, showing how the ROBS strategy can lead to significant tax savings.

Exit Strategy Costs: Insights into the expected costs of an exit strategy were shared, helping attendees plan for the future and understand the long-term financial implications of their investment.

The Value of Personalized Consultation

As the webinar concluded, DRDA offered attendees an exclusive opportunity for a complimentary one-hour consultation. This personalized advice is invaluable for individuals seeking to tailor the ROBS strategy to their specific circumstances. Such consultations can address unique challenges and provide customized solutions, further enhancing the appeal of the ROBS strategy.

Stay Connected

For those with additional questions, the speakers provided direct contact details. Bryan’s email and phone number were shared, along with a link to schedule a consultation. “We’re here to help you on your journey,” Doug assured, his sincerity resonating through the screen.

Bryan Uecker: bryan.uecker@drdacpa.com | 281-954-6004

Schedule a Consultation: Complimentary One-Hour Consultation

Final Thoughts

As the webinar concluded, there was a sense of accomplishment and excitement. The attendees had gained valuable insights into the ROBS journey, feeling more empowered to take the next steps in their entrepreneurial endeavors. The DRDA team was grateful for the opportunity to share their expertise and looked forward to continuing to support these aspiring business owners.

Thank you to all who joined us. Stay tuned for more from DRDA as we continue to help unlock success in entrepreneurial journeys.

- Published in ROBS 401(k), ROBS 401k Provider, Small Business, Starting a Business

Harnessing the Advantages of the ROBS / BORSA Structure.

PART I: C-CORP

By: Bryan Uecker, QPA, QPFC, AIF, AIFA

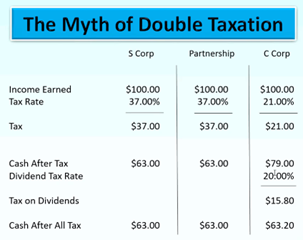

ROBS (Rollover as Business Start-up) or BORSA™ (Business Owners Retirement Savings Account) structures are exclusively compatible with C-Corps. This is because only C-Corps permit a 401(k) profit-sharing plan to serve as a shareholder. Upon discovering this exception, some prospective clients may feel disappointed, as the C-Corp often carries a stigma of “double taxation”. Historically viewed as “the entity choice of last resort” due to potential for double taxation resulting from corporate-level taxes and subsequent taxation upon distribution or liquidation. The good news is that C corporations present unique tax advantages that S corporations and partnerships cannot replicate.

To debunk the stigma of “double taxation” right up front, a helpful chart compares the corporate tax and dividend tax to profits through a pass-through entity at a personal tax rate of 37%:

So the issue is not how many times you are taxed……but rather how much tax you pay.

Now that we have cleared up the myth, here are ten benefits of a C-Corp:

1. Lowering Overall Tax Burden: C Corps can achieve significant tax savings thanks to a single flat corporate tax rate of 21%. By proactively managing dividends and salaries, business owners can optimize their tax burden, generally resulting in lower overall taxes than pass-through entities.

2. Flexible Fiscal Year: C Corps can choose their fiscal year, unlike LLCs and S Corps. This allows for better timing of income recognition and expense deductions, enabling shareholders to further minimize their tax burden.

3. Retaining Earnings for Growth: C Corps can reinvest profits within the company at a lower tax cost. Unlike S Corps, where profits are passed through to shareholders and taxed regardless of distribution, C Corps can retain earnings to fuel future expansion without immediate tax consequences.

4. Deducting Salaries and Bonuses: Shareholders of C Corps can receive salaries and bonuses, which are deductible expenses for the corporation. Businesses can optimize tax efficiency and mitigate double taxation concerns by structuring compensation packages appropriately.

5. Tax Write-offs for Fringe Benefits: C Corps can deduct 100% of medical premiums and other fringe benefits provided to employees. This includes health, long-term care, and retirement plan contributions, offering substantial tax savings opportunities for the corporation and its employees.

6. Charitable Contributions Deduction: C Corps can deduct charitable donations as business expenses, subject to certain limitations. This benefits worthy causes and provides tax advantages for the corporation, with the option to carry over excess contributions to future tax years.

7. Gaines: C Corps are taxed at a flat 21% on short-term and long-term gains so you no long have to carry economic risk to get to a lower tax bracket. You sell you capital asset when it is best for you. C Corps can carry forward capital and operating losses indefinitely to offset future profits. This flexibility allows businesses to smooth out tax liabilities over time, particularly during growth or economic downturns.

8. Fewer Ownership Restrictions: Unlike S Corps, which have strict ownership rules, C Corps can have unlimited shareholders, issue multiple classes of stock and be owned by anyone or anything. This flexibility facilitates equity financing and business expansion without the constraints imposed by S Corp regulations.

9. Favorable Treatment for Passive Investors: Passive investors in C Corps benefit from the inability to pass losses through to individual tax returns. Unlike S Corps, where active participation is required to claim losses, passive investors can still enjoy tax advantages without direct involvement in management.

10. Unique Financing Opportunities: Registering as a C Corp opens doors to diverse financing options, including public offerings and innovative strategies like 401(k) business financing, such as ROBS or BORSA™ plans. These financing avenues give businesses access to capital while minimizing debt obligations, offering a valuable alternative to traditional lending sources.

With over four decades of experience, DRDA, LLC has focused on supporting entrepreneurs in initiating, expanding, and selling their businesses. Leveraging our proficiency in accounting, business consulting, and retirement plan design, we harness the advantages of the ROBS/BORSA™ structure to benefit our clients throughout the operation of their business and at their succession transition or exit of their business, not just at formation.

By: Bryan Uecker, QPA, QPFC, AIF, AIFA

- Published in Business Lending, ROBS 401(k), ROBS 401k Provider, Small Business, Starting a Business

Discovering Financial Excellence: Why DRDA’s Tailored Solutions Stand Out

By: Eva Jiang, M.B.A., M.S.

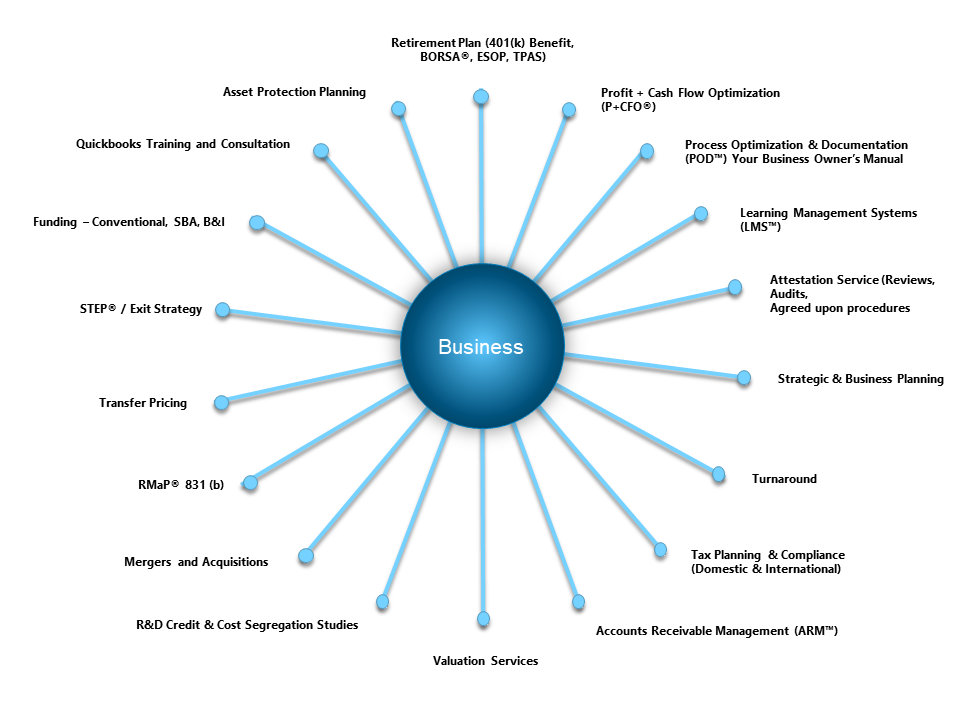

Looking for financial services that exceed expectations? Look no further than DRDA. Our comprehensive range of services encompasses tax planning and compliance, audit, accounting, bookkeeping, QuickBooks, 401(k) plan, Third Party Administration, BORSA® implementation, Operation and Exit, Profit and Cash Flow Optimization (P+CFO®), and Business Value Acceleration.

DRDA Wheel of Services

Because of our commitment to professionalism and uniqueness, we offer several trademarked services, including RMaP, BORSA, STEP, P+CFO, ARM, POD and LMS. At DRDA, we pride ourselves on our ability to make a difference in our clients lives. These trademarked services represent our dedication to providing cutting-edge solutions that are tailored to the needs of each client.

When you choose DRDA, you’re not just getting cookie-cutter solutions. Our team understands that every business is unique, which is why we take the time to truly understand your individual needs. We believe in open communication and collaboration across departments, ensuring that your experience with us is seamless and efficient.

Our tax services cover everything from planning and compliance to resolution, helping you navigate complex tax laws to minimize liabilities and maximize savings.

Our accounting services are tailored to your specific needs, providing accurate and reliable financial reporting. From auditing, assurance and financial statement preparation to budgeting and forecasting, our team helps you understand and trust your business information systems.

Our bookkeeping services ensure that your financial records are organized and up-to-date, allowing you to focus on what you do best – running your business. And if you use QuickBooks, our consultants can optimize your software usage, from setup and customization to training and ongoing support.

In addition to traditional services, our business advisory team offers strategic guidance to drive growth and profitability. Whether you need help with TPAS (Third-Party Administrative Services), retirement plan, BORSA® implementation (ROBS), business planning, performance analysis, or risk management, we’ve got you covered.

At DRDA, we don’t believe in a one-size-fits-all approach. DRDA Business Solutions are tailor-made for your business, saving you time and money while ensuring maximum efficiency and effectiveness.

Of the more than 46,000 CPA firms in the United States, DRDA has been recognized as one of the Top 500 CPA Firms in the United states by Inside Public Accounting, DRDA is ready to serve you. Visit our website at www.drdacpa.com to learn more about how we can help you and your business succeed and thrive.

By: Eva Jiang, M.B.A., M.S.

- Published in P+CFO™, ROBS 401(k), ROBS 401k Provider, Small Business, Starting a Business, Tax

Finance Your New Business During the Pandemic

BORSA, finance your new business during the pandemic

How can you make BORSA work for you? Now may be a great time to explore ROBS, or the Rollover Business Startup Solution and what it can do for you during the pandemic.

Key Points

- Start a new business or franchise

- Legally pay yourself a salary

- Abide by IRS and ERISA guidelines

What is the BORSA Plan?

The BORSA (Business Owners Retirement Savings Account) is DRDA’s, LLC Solution otherwise known as ROBS (Rollover Business Startup Solution), an IRS and ERISA approved structure that allows investors to use their retirement funds for a new business or franchise that they will be personally involved in. It is the primary way a retirement plan holder can have personal involvement in a business utilizing their retirement funds, without triggering IRC prohibited transaction rules.

Setting up a BORSA Plan requires planning but can be accomplished in relatively few steps.

- Set up a C Corporation – The process begins by establishing the new corporation, using the proper legal structure to support the establishment and operation of the company’s qualified retirement plan.

- Rollover your funds – Transfer your funds from an old IRA or 401(k) plan into a new 401(k) plan that the stock of the start-up C corp. business sponsors or adopts.

- Start earning a salary – You must be an employee of your new business and provide a legitimate service. Your compensation must come from your business.

How Do BORSA and Pandemic Relate?

While there’s a pandemic, millions are losing their jobs and joining the ranks of the unemployed. More than ever, many are trying to rely on themselves and not some corporate entity that must make difficult decisions to comply with federal and state mandates affecting individual earning, security, and livelihood. Using BORSA can be an ideal way to start the business of your dreams with money you already have.

BORSA can help you fund a new business or franchise with retirement funds, and that means you’re starting on your way to owning and fulfilling your goals. When COVID-19 hit, no one could have anticipated it would bring the unprecedented upheaval of everyday life that it has.

How Does BORSA Work?

The BORSA Plan allows an investor to create a C Corporation, and the C Corp’s profits are taxed separately from the owner as it is owned by shareholders. Next, funds are transferred from an old IRA or 401(k) plan. Then, as an employee providing a legitimate service, you are able to earn a salary at the business you’ve created.

There are very specific IRS and ERISA rules that have to be followed, and for this reason guidance is recommended. DRDA, LLC can help you get started. When it’s time for your new company’s stock to get valuated by the IRS, DRDA, LLC will help value the stock of the new or existing company.

BORSA Benefits

More than almost anything else, Americans are looking to make certain they can make it through the pandemic, civil unrest, and the whole of the current situations currently embroiling the nation. For those who have lost their jobs and have been unable to find replacement work, tapping into their retirement funds have been one source of income to help. But what happens when the funds have been depleted?

More than just taking funds out, though, BORSA can help you open a franchise or start a new business you can own yourself. Your money is helping you and your family first. The primary benefit of using the BORSA Plan is that you can employ it to use your retirement funds to invest in a business you will be personally involved in. You can do this without paying tax on the retirement funds you wish to use as a distribution.

Additionally, investing in yourself within your retirement portfolio is an excellent way to diversify. Your investments in traditional assets such as stocks and bonds, and alternative assets such as cryptocurrency, exist separately, and you can fund your own business as well. This may protect investment portfolios as a whole during times of unrest and market volatility,

During the COVID-19 and now the Delta Variant financial crisis, it’s important to know where your money is and what it’s doing. While investing in the market and traditional assets can bring you financial success, it’s very volatile at this time. Alternative assets like real estate can help diversify your portfolio. And using the BORSA Plan to fund your dreams can help you even more.

If you are interested in receiving more information on the BORSA™ plan, DRDA, LLC will be hosting a webinar on September 8th and 9th, 2021.

Click Here to sign up and access this FREE webinar.

- Published in Business Lending, ROBS 401(k), ROBS 401k Provider, Small Business, Starting a Business, Uncategorized

Using 401(k)/IRA Funds to Start or Buy a Business

Using Rollovers for Business Start-ups (ROBS) such as DRDA’s, LLC BORSA™ Plan

to finance a business isn’t new, but it is unfamiliar to many. As a result, there are a lot of myths swirling around about the use of ROBS structures that may be stopping would-be entrepreneurs from chasing their dreams.

BORSA Plans involve using money from an eligible retirement account to finance the purchase of a business or franchise. To summarize, a corporation is formed, and that corporation then sponsors a 401(k) plan. Funds are rolled from an existing retirement account into the new 401(k) without triggering a taxable distribution. This new 401(k) purchases (or invests in) shares of the corporation, which can then purchase a business or franchise.

In essence, a BORSA™ Plan allows you to invest in your own business where you have control rather than investing in the market where you have no control. Here’s the truth behind the most common ROBS myths:

- It’s not tax avoidance.

Using a BORSA™ Plan isn’t a way to evade taxes by any means. The Employee Retirement Income Security Act of 1974 (ERISA) was set up explicitly to encourage investment in small businesses – businesses that pay taxes. - BORSA™ Plan is an investment, not a loan.

With a BORSA™ Plan, you’re investing in your new business or franchise, not taking on debt. This means you won’t have to make monthly loan payments or incur interest. - You can use a BORSA Plan to diversify your nest egg.

You don’t have to take every penny from your existing retirement fund for a BORSA™ Plan to work. Many people only use a portion of their retirement assets, and this arrangement can be used in conjunction with a small business loan or other financing option. So, you can diversify your investments. - Getting funded using a BORSA™ Plan can take as little as four weeks.

Depending on the state in which you’re filing, and how fast you’re able to file the necessary paperwork, funding can take as little as a few weeks. Most are completed in less than 30 days. - BORSA Plans are not the same as Self-directed IRAs.

While it’s possible to finance a business with both self-directed IRAs and a BORSA™ Plan, there are some major differences between the two. If you use an SDIRA, the owner may not work for the business or take a salary. The investment amount is also potentially liable for the unrelated business income tax (UBIT), which can get very expensive. With the BORSA™ Plan, the 401(k) owner must work for the new business, and UBIT doesn’t apply. - A BORSA™ Plan can be used to fund start-ups.

A BORSA™ Plan is a great option to finance not only start-ups, but also purchases of existing businesses and franchises.

To some, the BORSA process can appear to have complex rules and regulations. But if you have a qualified retirement plan with a balance that’s sufficient for your start-up needs and work with an experienced company to support its formation, it can be a great option to start or re-capitalize your business debt-free.

Are you interested in learning more about DRDA’s, LLC ROBS structure, the BORSA™ Plan? Give our experienced team a call today 281-488-2022 for a free consultation

- Published in ROBS 401(k), Small Business, Starting a Business, Tax, Uncategorized

How to Use Retirement Funds, Tax and Penalty Free, to Purchase a Business

For most entrepreneurs, the most difficult part of starting a business is not coming up with an idea but financing the start-up. Over the past few years, many lenders have tightened their requirements for small business loans, leaving some would-be owners out in the cold. Another option is available, namely using your retirement funds to finance a business startup or providing the equity lenders need to make a loan.

In most instances using retirement funds will incur taxes and penalties, however there are three ways in which you can avoid both:

- Using a Roth IRA if you are over age 59 and the Roth IRA has been open at least five years

- 401(k) Loan Option

- Using a BORSA plan also known as Rollover on Business Startup Solution (ROBS)

Roth IRA

Taking a Roth IRA distribution may not be the most efficient way to fund a business, but it does have a potential advantage as it could help avoid taxes on the gain from the money used.

401(k) Loan Option

Some 401(k) plans allow you to borrow against your retirements account. This feature works well only if a small amount of money to start a business is required. Plans with this option allow participants to borrow the lesser of $50,000 or 50% of the vested value of your plan assets. The loan must be fully repaid within five years, via payments that are at least quarterly, at market interest rates.

ROBS

ROBS is the most flexible way to fund a fledgling business. To understand this structure you have to understand provisions of the Employee Retirement Income Security Act (ERISA) and the Internal Revenue Code (IRC). The plan should be approved by both the Department of Labor (DOL) and the Internal Revenue Service (IRS). This approval comes in the form of a Favorable Determination Letter from the IRS.

This method is a great way to fund a business, especially if more than $50,000 in a qualifying retirement account is available. If less than $50,000 is available, taking a loan against the investment may be a better option. ROBS may be used for business acquisition, working capital or as a down payment for additional financing. If you meet the criteria, it is usually the most cost-effective method, plus there is no requirement to repay the money especially in those early years of operation.

Setting up a ROBS involves rolling over a pre-tax IRA or 401(k) plan account into a new 401 (k) sponsored by a “C” Corporation. The rollover funds are then invested into the stock of the “C” Corporation. The account holder can then earn a reasonable salary as an employee of the business.

Starting or buying a new business is complicated. Using your retirement money to fund a business is a viable option but also adds a layer of complexity that you need to understand. Your best plan of action before you do anything is to consult with someone who understands the pros and cons of each of these options. DRDA, PLLC – CPAs has provided these services to thousands of entrepreneurs and we would be happy to discuss this option and help you determine what method works best for you. Contact us to learn more about BORSA (Business Owner’s Retirement Savings Account), our exclusive ROBS plan that allows investors to access their 401(k) funds tax and penalty free.

- Published in ROBS 401(k), ROBS 401k Provider, Starting a Business

How to Finance a Business with an SBA loan and Retirement Funds

Entrepreneurs seeking to finance a startup company often look to the Small Business Administration (SBA) for the funding they need to get their company up and running. One of the most beneficial ways to get the funds needed is to use a 401(k) financing, also called a Rollover on Business Startup (ROBS), in conjunction with an SBA loan. The ROBS process allows the borrower to leverage retirement funds without incurring any tax or penalties. SBA loans and ROBS have advantages as stand-alone instruments but when they work in conjunction with one another, they can provide even greater buying power and flexibility

Advantages of SBA Loans

The SBA generally does not make direct loans to entrepreneurs. Rather, it provides a guarantee to lenders for the money they loan to start the business. This guarantee protects lenders by promising to pay the loan if the business owner defaults. SBA loans are a popular form of financing because the interest rate is lower, typically 6% to 9% and offer longer repayment terms than other forms of financing. These loans do have qualification criteria starting with a required credit score of at least 680 along with a strong financial and industry experience history.

The SBA requires would-be business owners to have a minimum 10% down payment on all SBA loans, however, many lenders providing SBA loans may require a down payment of 20-30% of total startup coasts. For an average size loan, the down payment will be between $40,000 to $120,000.

How ROBS Helps to Secure an SBA Loan

ROBS allows entrepreneurs to use retirement funds to start or buy a business with money that has been invested in a 401(k), IRA or other qualified account as a down payment for an SBA loan without triggering any tax penalties. Using a ROBS account to fund your down payment also makes it easier to qualify for an SBA loan As long as you have at least $50,000 in a retirement account that can be rolled over in a ROBS account you may qualify for this type of funding.

When you combine a ROB account with an SBA loan, you’ll access capital from two different sources, thus reducing the amount needed from each. You’ll save money on interest and reduce your monthly payment. Securing a loan with ROBS can allow you to become debt-free sooner, putting you on the road to profitability.

Make ROBS Management Easy With Our BORSA Plan

Funding your business with a ROBS account requires several necessary steps, including the establishment of a “C” Corporation. Ongoing management is also necessary to ensure that you remain in compliance with all regulations (i.e. DOL, IRS, etc.). DRDA’s BORSA (Business Owner’s Retirement Savings Account), an exclusive ROBS plan that allows investors to access their 401(k) tax and penalty free will help set up your financing and perform the necessary ongoing work to make sure you remain in compliance with all ROBS requirements. Contact DRDA for more information and a consultation.

Contact us to learn more about BORSA (Business Owner’s Retirement Savings Account), our exclusive ROBS plan that allows investors to access their 401(k) tax and penalty free.

- Published in ROBS 401(k), ROBS 401k Provider, Starting a Business

- 1

- 2