Delving into Required Minimum Distributions (RMDs) for 401(k) Plans: Understand the New Rules

By Bryan Uecker, QPA, QPFC, AIF, AIFA

A Required Minimum Distribution (RMD) is the mandated withdrawal amount from certain retirement accounts on an annual basis after reaching a specific age. These rules were established by the government to prevent retirement accounts from being used solely for estate planning purposes to transfer wealth to beneficiaries upon the account holder’s death. It’s crucial for participants in 401(k) plans to grasp these regulations as failure to comply with RMD requirements can lead to tax penalties imposed by the IRS.

Understanding the “Required” Aspect of RMDs:

An RMD must be distributed from your 401(k) account each year once you reach a designated age. However, if you’re still employed when you reach this age, your plan might allow you to postpone RMDs until retirement.

RMD Age or Retirement:

The age for commencing RMDs is determined by your birth year:

– Born before July 1, 1949: RMD age is 70 ½

– Born after June 30, 1949, and before January 1, 1951: RMD age is 72

– Born in 1951 through 1959: RMD age is 73

– Born after 1959: RMD age is 75

However, you might be able to defer your initial RMD beyond this age if you’re still employed by the plan sponsor and don’t own more than 5% of the business. Owners with more than 5% ownership must start RMDs at the designated age.

RMD Deadline:

Typically, you must receive the RMD by December 31 of the relevant year. However, the first RMD can be delayed until April 1 of the following year if it’s the later of reaching RMD age or retiring (if allowed by the plan and you’re not a 5% owner).

RMDs Upon Death:

Regardless of whether you’ve reached RMD age, distributions must be made from your 401(k) account upon your death. Beneficiaries usually have ten years to withdraw the full amount, though some, like spouses or minor children, might be eligible for extended payment periods.

RMDs with BORSA®:

For many BORSA® clients, employer securities make up the bulk of their 401(k) balance. The corporation can repurchase shares to cover the RMD, or the participant can opt for an “in-kind” distribution in employer securities equivalent to the RMD’s fair market value. The participant is subject to ordinary income tax on the in-kind distribution and holds the stock personally.

RMDs and Roth 401(k) Accounts:

Starting with the 2024 RMDs, Roth 401(k) accounts are not subjected to the same RMD rules. Prior to 2024, Roth 401(k) accounts followed the same rules but were non-taxable.

By Bryan Uecker, QPA, QPFC, AIF, AIFA

- Published in ROBS 401(k), ROBS 401k Provider, Small Business

Forging a Bright Career Ahead: Empowering Students Through DRDA, LLC

By: Eva Jiang, M.B.A., M.S.

Success Starts Here

Bauer Connect: Bridging Futures – An event Recap

Last week, UH Bauer students had the opportunity of engaging with DRDA, LLC leaders from diverse backgrounds at the Bauer Connect event. The attendees experienced a dynamic lineup of presentations, participated in a lively quiz session, and engaged in a thought-provoking panel discussion, providing invaluable insights for their professional journeys.

Connecting with University and Campus:

Connecting with universities and campuses is crucial for companies like DRDA, LLC and the accounting industry. It not only allows us to share our knowledge and experience with the next generation of professionals but also provides an opportunity for students to gain real-world insights and build connections within the industry. Through events like Bauer Connect, we aim to foster a mutually beneficial relationship between academia and industry, empowering students to thrive in their future careers.

Opportunities for Growth:

For students considering their career paths, joining DRDA, LLC offers more than just a job—it’s an opportunity for growth and advancement. Unlike experienced staff who may have already established their careers, students have the advantage of a blank canvas, ready to be painted with diverse experiences and opportunities.

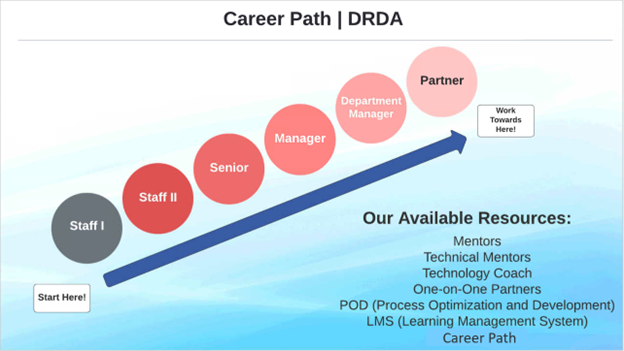

At DRDA, LLC we recognize and value the fresh perspectives and innovative ideas that students bring to the table, offering them a platform to shine and make meaningful contributions from day one. Take, for example, our tax department career path: starting as Staff I, graduates progress to Staff II and then to Senior positions. With dedication and skill development, they can advance to roles such as Tax Manager/Department Manager and ultimately become Partners at twice the industry norm. This advancement is made possible because of the resources DRDA, LLC has developed to help our people succeed. The picture below lists some of those resources. If you want to know more about these resources and the opportunity for you, just give us a call or email.

A Bright Future Awaits:

As students embark on their journey with DRDA, LLC they can look forward to a promising future filled with opportunities for personal and professional development and growth. Unlike many CPA firms, where partnership is often restricted to a select few, DRDA, LLC offers a rare opportunity for every member of our team to become a partner if they desire. We believe in treating everyone fairly and giving opportunities based on talent and hard work, ensuring that the brightest and most dedicated individuals have the chance to shape the future of our firm.

In conclusion, DRDA, LLC is dedicated to empowering students and shaping their bright futures. Join us as we bridge the gap between academia and industry, together forging a path to success.

By: Eva Jiang, M.B.A., M.S.

- Published in Culture, Team Achievement, Team Achievment