In the world of business entities

By Agustin Muniz

In the world of business entities, the C-Corporation (C-Corp) stands tall, offering a plethora of tax advantages that can significantly benefit entrepreneurs and shareholders alike. Although it may not be the perfect fit for every company, understanding the tax advantages of a C-Corp can make it an attractive option for those looking to maximize tax benefits and unlock potential growth opportunities.

- Lower Tax Rates: One of the most significant advantages of a C-Corp lies in its lower tax rates compared to other business structures. Unlike pass-through entities like S-Corps and LLCs, C-Corps are subject to their corporate tax rates. The current corporate tax rate can be more favorable for companies with substantial profits, providing an opportunity to retain more earnings for reinvestment.

- Flexible Deductions: C-Corps have the advantage of enjoying a broader range of deductions compared to other entities. They can deduct business expenses, employee benefits, healthcare premiums, retirement plans, and more. This flexibility in deductions can reduce the taxable income, resulting in substantial tax savings for the corporation.

- No Limitation on Ownership: Unlike S-Corps, C-Corps have no restrictions on ownership. They can have an unlimited number of shareholders, and there are no limitations on who can be a shareholder. This feature can be especially appealing for businesses planning to seek investments or go public in the future.

- Franchise Tax Benefits: Certain states offer more favorable franchise tax rates for C-Corps, reducing the overall tax burden on the company. For businesses operating in these states, opting for a C-Corp structure can lead to significant tax savings in the long run.

- Retained Earnings and Accumulated Profits: C-Corps can retain earnings within the corporation, allowing for the accumulation of profits for future expansion, acquisitions, or investments. While other business structures may require distributing profits to shareholders, C-Corps have the advantage of deferring distributions and minimizing tax liability.

- Stock Options and Employee Incentives: C-Corps can issue stock options and other equity-based incentives to employees. These offerings can be a powerful tool for attracting and retaining top talent, providing them with an ownership stake in the company’s success, while also offering tax benefits to the corporation.

It’s essential to note that C-Corps are subject to double taxation, as profits are taxed at the corporate level, and any dividends distributed to shareholders are taxed again at the individual level. However, the potential tax advantages and other benefits of a C-Corp structure often outweigh this drawback, particularly for businesses with ambitious growth plans and significant earnings.

Ultimately, the decision to choose a C-Corp should be based on a comprehensive evaluation of the company’s specific financial goals, tax strategy, and long-term vision. Consulting with a qualified tax advisor or legal professional is crucial in making the right choice, ensuring that a C-Corp is the best fit for the business’s unique needs and objectives.

- Published in Job Posting

Three reasons business owners should consider Cash Balance Plans

By: Bryan Uecker

Over the last half-century, employers shifted most of the retirement plans away from employer-funded pension plans (defined benefit) to employee/employer-funded savings plans such as the 401(k) (defined contribution). Defined contribution plans continue to eclipse defined benefit plans by an ever-widening margin when considering the number of plans and total assets. However, one defined benefit plan is getting some recent attention: the Cash Balance Plan. Here are three reasons why:

1: Business owners can accumulate more for retirement and reduce current taxes.

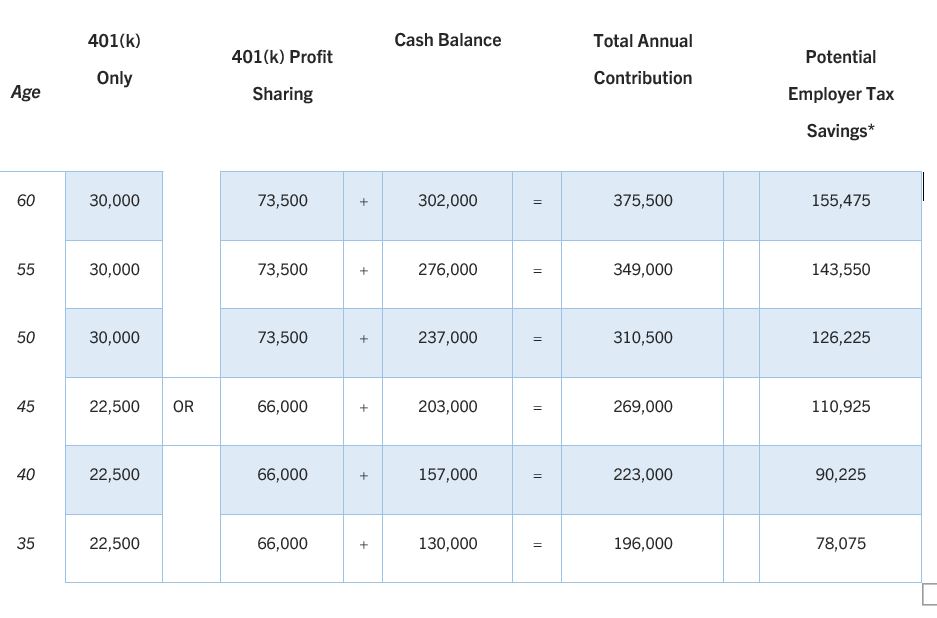

The biggest attraction of a cash balance plan is that key employees can typically contribute more – often much more – to the plan. Look at the following table. A 60-year-old owner or key employee could contribute up to $30,000 in 401(k), or up to $73,500 if the 401(k) has a profit-sharing component. Adding the cash balance to the 401(k)-profit sharing plan would allow total employee and employer contributions of up to $375,500.

Moreover, employer contributions are deductible for the business. This means an employer could have saved over $155,000 in taxes on that same 60-year-old.

2023 contribution limits. 401(k) limit includes annual catch-up contributions for participants aged 50 or older. For illustrative purposes only. Actual results may vary depending on the plan design, participant compensation, employee demographics, and projected retirement age.

*Based on assumed combined federal and state tax rate of 45%. Calculation uses “Total Annual Contribution” excluding 401(k) contributions.

2: Easy to understand and portable.

A cash balance plan is a defined benefit plan in which an employer credits a participant’s account with a “pay credit” (a percentage of pay or a flat dollar amount) and an “interest credit” (either a fixed or a variable rate). The lumpsum benefit at retirement equals the “account balance” which is the accumulation of all annual pay and interest credits. To the participant, it looks and feels like an interest-bearing savings account with annual deposits and earnings.

In a traditional defined benefit plan, the “goal” or the “what” that’s being defined is a monthly pension amount payable for life at retirement age. The annual funding needed is based on whatever amount it takes to accumulate enough to pay out the promised benefits on the promised retirement dates. It’s not rocket science, but it takes an actuary to determine the present value of all future benefits and compare it with the plan’s current assets. The actuary must make assumptions about current and future interest rates, mortality, turnover, inflation, salary increases, etc.

In a cash balance plan, the present value of benefits is in the ballpark of the sum of the “account balances”. The annual contribution is in the ballpark of the sum of the “pay credits” for the year. The actuary keeps a tally of how the plan assets fare in reality compared to the “interest credit” for the year and adds plus or minus to the mix.

The cash balance plan is portable. Most defined benefit plans have a default payment of an annuity for life, the default payout for most cash balance plans is a lump sum that can be rolled into an IRA.

3: Allows for multiple employee groups with different contribution rates.

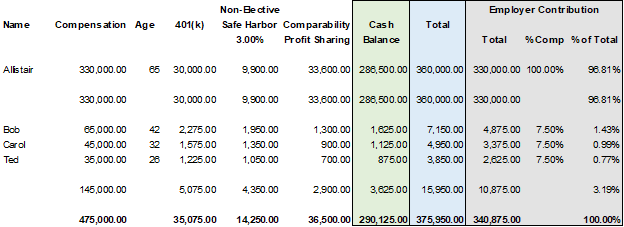

A cash balance plan works beautifully with a “new-comparability” or “cross-tested” profit sharing plan. Because a cash balance plan can be combined with a profit sharing plan for non-discrimination testing, employers with a cross-tested profit sharing typically requiring an allocation of 5% of compensation to non-highly-compensated employees in order to max-out contributions to key employees, can supercharge the amounts to key employees while sometimes only raising contribution requirements to non-highly-compensated employees by 2.5%.

2023 contribution limits. 401(k) limit includes annual catch-up contributions for participants aged 50 or older. For illustrative purposes only. Actual results may vary depending on the plan design, participant compensation, employee demographics, and projected retirement age.

Please note that for certain plans that are not covered by the PBGC (e.g., owner-only/spouse plans and certain professional services businesses, etc.), employer contribution amounts to a 401(k)/profit sharing plan may be limited to an IRS deduction limit of 6% of total eligible compensation.

In the above scenario, the non-highly compensated employees can defer up to the maximum 401(k) contribution of $22,500. They all receive employer contributions totaling 7.5% of compensation made up of a 3% non-elective safe harbor, a 2% profit sharing, and a 2.5% cash balance. The owner can defer $30,000 in 401(k), including a $7,500 catch-up. In addition, he can receive an employer contribution equal to 100% of compensation made up of a 3% non-elective safe harbor, ~10% profit sharing, and ~87% cash balance.

Frequent questions about cash balance plans.

Aren’t fees to administer cash balance plans expensive? The annual 5500 requires an attachment called Schedule SB which reports the funding adequacy of the defined benefit plan. An enrolled actuary must certify the figures and assumptions on the form. The need for an actuary adds a cost for cash balance plans that isn’t needed for most defined contribution plans. However, because the cash balance plan is usually valued once a year by the actuary and TPA (Third Party Administrator), and the assets are pooled, there is no need for a third-party recordkeeper, and the investment fees are typically lower than 401(k) plans.

Are annual contributions to a cash balance plan mandatory? Except for safe harbor plans, contributions to a defined contribution plan are usually discretionary meaning if the employer chooses not to contribute every year they don’t have to. For the cash balance plan, the actuary will calculate a minimum and maximum funding range every year and the employer must meet at least the minimum funding requirement.

What is the deadline to set up a new cash balance plan? Before 2020, a new cash balance plan had to be adopted by the last day of the plan’s first year. Thanks to the SECURE Act, business owners can adopt a cash balance plan until the entity’s tax filing deadline (including extensions) for the plan’s first year. Because of the time needed to prepare the plan document, calculate the required contribution, and fund the contributions to the trust by the deadline, however, plan on a couple of months lead time.

Can a cash balance plan use a vesting schedule? Yes. Most plans use a “three-year cliff” vesting schedule. 0% vested for years one and two and 100% vested with three years of service.

Why DRDA? DRDA has spent decades developing real world solutions to everyday business issues. As technology, resources and awareness change, our solutions are updated, introduced or replaced to make certain we offer the best solution today. DRDA takes a holistic view of the business owners’ situation including a comprehensive financial and tax strategy – encompassing both personal and business. We offer integrated solutions that save time and money such as bookkeeping, payroll, and retirement plans. This is all in service of creating better futures for our clients. Where do you want to go from here? Let us help you get there.

For an illustration call (281) 488-2022 or email bryan.uecker@drdacpa.com.

- Published in ROBS 401(k)

A robust and efficient payroll system is a vital component of any successful business.

By: Agustin Muniz

A robust and efficient payroll system is a vital component of any successful business, regardless of its size. The significance of utilizing a payroll system cannot be overstated, as it not only ensures accurate and timely payment to employees but also streamlines various critical aspects of human resources and financial management. Here are some compelling reasons why businesses should prioritize the implementation of a reliable payroll system:

- Accuracy and Compliance: Payroll systems automate the payroll process, reducing the risk of human errors in calculations. By accurately computing wages, taxes, and deductions, businesses can avoid costly mistakes and maintain compliance with ever-changing labor laws and tax regulations.

- Time and Cost Savings: Manual payroll processing can be time-consuming, diverting valuable resources away from core business activities. A dedicated payroll system automates repetitive tasks, saving time and allowing HR and finance teams to focus on strategic initiatives and employee development.

- Enhanced Data Security: Employee payroll data is sensitive and must be safeguarded. Payroll systems incorporate robust security measures, protecting confidential information from unauthorized access and potential breaches, thus mitigating the risk of data theft and legal ramifications.

- Employee Satisfaction and Retention: A timely and accurate payroll process boosts employee morale and satisfaction. By ensuring employees are paid accurately and on time, businesses create a positive work environment and foster higher levels of employee loyalty and retention.

- Improved Reporting and Analytics: Payroll systems provide comprehensive reporting capabilities that enable businesses to gain insights into labor costs, tax liabilities, and other financial metrics. Such data-driven insights empower businesses to make informed decisions and devise effective strategies for growth and profitability.

- Seamless Integration: Many modern payroll systems can seamlessly integrate with other HR and financial software, streamlining data flow and eliminating data silos. This integration enhances overall operational efficiency and data accuracy throughout the organization.

- Scalability and Flexibility: A good payroll system can adapt to the evolving needs of a growing business. As the organization expands, the payroll system can accommodate new hires, additional benefits, and complexities without disrupting the payroll process.

In conclusion, implementing a reliable payroll system is not merely an option for businesses but a necessity. The advantages it offers, such as accuracy, cost savings, data security, employee satisfaction, and operational efficiency, make it an indispensable tool in today’s competitive business landscape. By investing in a robust payroll system, businesses can streamline their operations, reduce administrative burdens, and focus on their core competencies, ultimately driving growth and success in the long run.

By: Agustin Muniz

- Published in ROBS 401(k)

What is ERISA and how does it benefit your business?

By: Agustin Muniz

The Employee Retirement Income Security Act (ERISA) is a significant federal law that sets standards for employee benefit plans offered by private employers. Enacted in 1974, ERISA aims to protect the rights and interests of employees who participate in retirement plans, health insurance programs, and other welfare benefit plans. ERISA was enacted to establish minimum standards for employee benefit plans to safeguard the financial security and welfare of employees. It applies to private-sector employers that offer employee benefit plans, including pension plans, 401(k) plans, health insurance plans, and other welfare benefit plans. ERISA does not cover government plans, church plans, or plans maintained outside the United States for non-resident aliens.

One of the central aspects of ERISA is the imposition of fiduciary standards on those who manage and control employee benefit plans. Fiduciaries, such as plan administrators, trustees, and investment managers, are legally obligated to act in the best interests of the plan participants and beneficiaries. They must exercise prudence, loyalty, and diligence in managing the plan and its assets. ERISA mandates various reporting and disclosure requirements to ensure transparency and accountability in employee benefit plans. Employers are required to provide plan participants with essential information, including plan features, funding mechanisms, investment options, and potential risks. This includes distributing Summary Plan Descriptions (SPDs), Summary Annual Reports (SARs), and other disclosures to participants. ERISA includes provisions that protect employees’ rights to their accrued benefits. The law establishes rules for vesting, which determines when employees become entitled to receive their full pension benefits. Additionally, ERISA created the Pension Benefit Guaranty Corporation (PBGC), a federal agency that provides a safety net by insuring certain pension benefits in case of plan termination.

ERISA provides mechanisms for enforcing compliance and addressing fiduciary breaches or plan violations. The law grants authority to the Department of Labor (DOL) to oversee and enforce ERISA provisions. Participants and beneficiaries also have the right to bring lawsuits to enforce their benefits and seek remedies for fiduciary breaches or other violations of ERISA.

ERISA has had a profound impact on employee benefit plans and the retirement landscape in the United States. It has helped establish standards of conduct for fiduciaries, promote transparency in plan administration, and provide avenues for legal recourse in case of misconduct. ERISA has also facilitated the growth of retirement savings plans like 401(k) plans, providing individuals with tax advantages and investment opportunities to build their retirement nest eggs. The Employee Retirement Income Security Act (ERISA) serves as a crucial framework for regulating private-sector employee benefit plans, ensuring the protection of employees’ rights and interests. By establishing fiduciary responsibilities, reporting requirements, and benefit security measures, ERISA promotes transparency, accountability, and the long-term financial security of plan participants. Understanding the key provisions of ERISA is essential for both employers and employees to navigate the complex landscape of employee benefits effectively.

For more information on ERISA and how DRDA, LLC can help please click here.

- Published in ROBS 401(k), Uncategorized